What’s an Upside Down Car Loan & How Do You Get Out of It?

What’s an Upside Down Car Loan & How Do You Get Out of It?

Posted on February 1, 2024

Nobody likes going upside down on a loan. It’s an uncomfortable feeling and even if you have no intention of selling your car in the near future, it’s not a position anyone wants to be in.

So what can you do about it?

What's an Upside Down Car Loan?

Going upside down is also referred to as negative equity. That’s when the amount of your car loan is more than the value of your car. It’s a position some borrowers find themselves in after buying a new car.

It doesn’t last forever but it can be an uncomfortable time. So, what can you do about it?

Things You Can Do About an Upside Down Car Loan

Larger down payment: You can help prevent going upside down in a car loan by putting down a larger down payment. It offsets that initial dip of depreciation that comes with a new car and puts you ahead of the game.

It isn’t always possible to put down a bigger down payment but can be a good idea if you can save enough.

Overpay your loan: Many car loans have an overpayment facility where you can pay more each month or pay a lump sum off the loan. Make sure the amount comes off the principal, the amount owed rather than the interest and you can even things out over time.

Not all car loans can be overpaid so check your loan paperwork or talk to your lender to make sure.

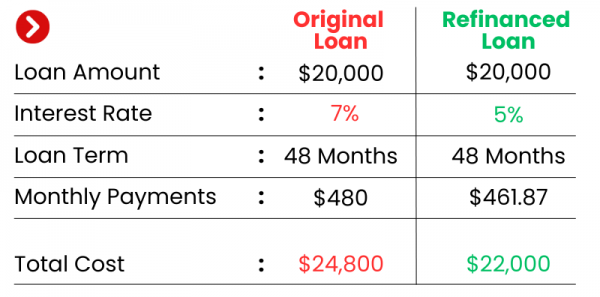

Refinance the car loan: If you cannot overpay, you may benefit from refinancing the loan. Depending on your circumstances, you could go shorter with higher payments. You could also add a lump sum to overcome the negative equity.

You have to be careful with refinancing to offset the negative equity somehow. That is easiest done with the payment you would have used as a lump sum had your current lender been willing to accept it.

Sell the car: This isn’t always the best option but it is an option. If you’re paying for a second car or a higher-value car, you could sell it and add a lump sum to pay off the debt. This depends on you being able to save enough for that lump sum in the first place but is an option.

Do nothing: The easiest thing to do is continue paying the upside-down car loan and not worry about being upside down. It’s only relevant if you’re planning to sell or replace the car in the near future. If you’re planning to keep the car and pay off the loan, it doesn’t matter if you’re upside down for a few months.

Negative equity has no impact on your credit score or on your financial well-being as long as you make the payments on time.

It only makes a difference if you plan on trading in or buying a new car. If you’re not planning either of those things, it really doesn’t matter!

If you're ready for a car loan, we'd love to help with that! simply fill in the form below to get started.